I have been involved in the call center and customer engagement market for more than 25 years, first as a consultant and systems integrator and for the past 11 years as an industry analyst. There have been lots of changes in that time but never as many as in the last 12 to 18 months. A simple illustration of the change is how I group vendors.

In the early days I used three categories: telephony management, customer relationship management and workforce optimization. Telephony management included the on-premises ACD and PBX vendors such as Alcatel/Lucent, Avaya, Cisco and Nortel along with Genesys, which at the time was a specialist in computer/telephony integration and routing with products to receive calls from an ACD or a PBX and route them to a telephone extension based on predefined rules, and pop up predefined screens onto the agent’s desktop. CRM was dominated by three big vendors, Oracle, SAP and Siebel, plus some niche vendors such as Clarify and SugarCRM. WFO was emerging and was dominated by Aspect, NICE and Verint, which were building their portfolios through acquisitions and in-house development. All these vendors (except Siebel, acquired by Oracle) still exist but have added applications to their portfolios, expanded the scope of their original applications and/or have acquired other vendors.

Alongside these changes, the overall IT market has been disrupted by the emergence of new supply models, the need to support mobile devices and the advent of big data. In the first case the emergence and acceptance of cloud computing has forced vendors to adapt their product architectures and sometimes develop new products to offer services “in the cloud.” Mobile devices have become so ubiquitous that vendors have to support access to their systems through them, including text-based communications, and many have developed platforms that enable organizations to develop their own mobile apps. In the third major change, vendors developed systems that can process big data, including the vast volumes of unstructured data that organizations are generating in their new interaction channels, and some also developed analytics capabilities to make sense of all types of data. To reflect these changes, I expanded my vendor categories to five: contact center in the cloud, self-service, marketing, sales and services clouds, WFO and analytics.

The contact center in the cloud group includes vendors that developed telephony management systems (ACD and PBX, routing, CTI, IVR, call recording and interaction analytics) as software systems and moved to providing them as cloud-based services. Several evolved their products also to support other communication channels (email, text, chat, social media and mobile platforms). Thus began the transition to multichannel interactions and the potential for omnichannel engagement. Self-service includes vendors that support customer engagement that does not involve employees, such as visual IVR, advanced Q&A-style Web-based self-service, mobile apps, social customer service and social forums. The third group includes large CRM vendors that have split their previous on-premises, integrated CRM systems into marketing, sales and service clouds, and some niche vendors that supply integrated CRM as cloud-based services. In the fourth group, WFO also includes some niche and suite vendors that offer various combinations of interaction recording, quality management, workforce management, coaching and training, agent compensation management and agent-related analytics. In perhaps the biggest change, several specialist analytics vendors introduced analytics on structured data, voice recordings, text-based data, events and combinations of them. This has allowed organizations to get closer to having a “360 degree” view of the customer, journey maps, root-cause analysis and predictive capabilities. These groupings are not necessarily exclusive – many vendors have products that fall into more than one group, especially analytics. And of course, not all products include the same capabilities and may be delivered through different cloud models (private, public and hybrid). There are also some niche vendors that don’t fit in these groups,  offering products such as stand-alone agent desktop systems, customer feedback (which is beginning to be included with WFO) and gamification (also being included in WFO). Please visit our website to see a full list of the vendors we cover.

offering products such as stand-alone agent desktop systems, customer feedback (which is beginning to be included with WFO) and gamification (also being included in WFO). Please visit our website to see a full list of the vendors we cover.

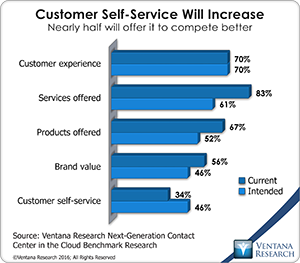

In recent times the market has undergone even more disruption as vendors try to support customer experience management, both through acquisitions and realigning their product portfolios. Our benchmark research into the next-generation contact center in the cloud shows that customer experience has become the number-one way organizations expect to compete for customers, and increasingly businesses attempt to do this by providing more channels of engagement and innovative self-service. The research shows that to help them, organizations are looking to vendors that have integrated portfolios of products. The bigger vendors are thus investing in more internal product development, greater integration of existing products, more support for cloud computing and mobility, and acquiring vendors that have complementary systems. For example, Aspect seems to have sorted out its financial situation and recently announced a new product, Aspect Via, that brings together previously disconnected channel management, self-service, WFO and analytics into a platform to support omnichannel engagement. Genesys also seems to have sorted out its finances and having already expanded from CTI and call routing to offer a multichannel contact center in the cloud, WFO and analytics, it recently announced the acquisition of Interactive Intelligence, which will add more contact center in the cloud options, such as ININ’s PureCloud Engage, to its portfolio. NICE has taken probably the boldest move by its acquisitions of Nexidia and inContact, which when brought together will support in my view a complete customer engagement suite of multichannel interaction management, self-service, advanced WFO, multidimensional analytics and integration with on-premises and cloud-based third-party applications. It has also expanded its portfolio by developing two new products aimed at organizations with smaller contact centers, a packaged WFO product and a packaged performance management product, thus allowing smaller centers to have access to similar but slightly more limited capabilities to larger centers. Verint has also continued its acquisitions, including Kana and Contact Solutions, giving it a portfolio of self-service, WFO, multidimensional analytics and integration with third-party CRM and contact centers in the cloud. All of these developments provide options that help organizations advance toward omnichannel customer engagement, through improved integration between systems and thus the ability to connect what have been disconnected processes.

Alongside these developments, it is hard to ignore what is happening in the CRM market. Oracle has split CRM into three clouds (marketing, sales and service), built them on a common platform for integration and data management, and supports them with customer and interaction analytics. However, in an illustration of just how fast this market is changing, at its recent OpenWorld event, Oracle provided a sneak preview of its new Engagement Cloud, which brings customer engagement onto a single platform. Salesforce has done the same CRM split, developed several other clouds, included self-service capabilities and analytics, and placed them on a platform that supports application development, integration and data management. SAP has been the quietest of the three but has moved CRM to the cloud and has a complete though hidden set of contact center capabilities. These moves change the CRM market, giving more support to three key business groups but potentially losing a single source and view of the customer. Some of the niche vendors such as SugarCRM have bucked this trend by keeping a single cloud product and adding capabilities to it.

Many vendors, in several categories and with highly variable capabilities, now market their services and products under the brand Customer Experience. So the question becomes what is customer experience and what systems do organizations need to support it? I believe that consumers’ expectations of customer experience in engaging with an organization are that it must be easy, personalized, in-context, consistent and accessible regardless of the channel, time of day or point of engagement. I have said before that no one system can deliver all of this. A complete experience requires a combination of channel management (assisted and digital), employee management (using WFO systems) and business applications, as well as analytics to tell users what is going on, possible consequences of actions and decisions, and what should be changed going forward. In their different ways the vendors in the customer experience market are striving to provide such capabilities, but it is an open question as to which of them will succeed. So far 2016 has been a year of major change, and there is more to come. As yet few vendors have taken the next steps to incorporate the Internet of Things (IoT) or Artificial Intelligence into their portfolios. I believe both of these technologies will impact customer experience: IoT allows organizations to collect even more customer data through a range of devices, and AI is used to make processes smarter, more efficient and more effective. So please stay tuned as I do my best to keep you informed of developments that will help you meet the ever increasing expectations of your customers.

Regards,

Richard J. Snow

VP & Research Director, Customer

Authors:

Ventana Research

Ventana Research, now part of Information Services Group (ISG), is the most authoritative and respected market research and advisory services firm focused on improving business outcomes through optimal use of people, processes, information and technology. Since our beginning, our goal has been to provide insight and expert guidance on mainstream and disruptive technologies. In short, we want to help you become smarter and find the most relevant technology to accelerate your organization's goals.