Accountants love electronic spreadsheets – and for good reason. They’re a powerful and versatile personal productivity tool and just about everyone knows how to use them. Spreadsheets are the default software tool for accountants because they enable autonomy (you don’t need to ask IT for anything) and they’re free (so you don’t have to make a business case to authorize buying something). Some accountants humorously (but earnestly) invoke the line “you’ll have to pry this spreadsheet from my cold, dead hands” whenever somebody suggests eliminating them.

There’s no reason to eliminate spreadsheets, but they’re not always the right choice for accountants. It will probably come as a shock to those in the profession but accounting standards have evolved past the point where spreadsheets are a useful tool for managing or supporting finance department processes. In particular, I’ve commented before on the impact of the new standards for revenue recognition for contracts and lease accounting.

Accounting departments worldwide are working overtime these days adapting to these new accounting standards. Accounting executives must understand that these new standards (ASC 842 for the U.S. and IFRS 16 elsewhere) have crossed a significant threshold. Whether they intended to or not, the Financial Accounting Standards Board (FASB), which establishes accounting standards for the United States, and the International Accounting Standards Boards (IASB), which does the same for most of the rest of the world, have created standards so complex that they demand modern accounting information systems to achieve reliable compliance. As a practical matter, spreadsheets cannot adequately handle the process, data management and collaboration requirements. This note focuses on lease accounting but my conclusion applies equally to revenue recognition.

To put the relationship between technology and lease accounting standards into a historical perspective (here I’m mainly focusing on U.S. history), it’s useful to recall that the absence of available technology when the issue was first raised a half-century ago was behind the decision not to recognize operating leases as formal obligations on balance sheets. In those days, business computing was in its infancy. Without computers or even inexpensive fax machines, collecting comprehensive data about, say, every leased copying machine or backhoe and then translating that information into a formal liability on the balance sheet would have been a significant burden. The need for a practical expedient along with heavy lobbying of the FASB by industry and commercial leasing companies relegated lease obligations to a company’s financial-statement footnotes.

Today’s senior corporate and finance executives have spent most of their careers in an era when spreadsheets could get accounting tasks done, albeit at an increasingly heavy cost in lost productivity as well as limited visibility into processes and data. It’s likely that these executives don’t appreciate that the new standards demand effective information technology for efficient compliance. That’s because the standards bodies didn’t put a warning label on them.

What would that warning label say? The new revenue and lease accounting standards require a significantly higher level of data collection and analysis than had been the case up until now. Companies must be able to reliably capture a wide range of financial and non-financial data related to the terms and conditions of the lease. Moreover, the new lease standards often require the use of complex models and formulas to assess the value of lease obligations. These characteristics make spreadsheets the wrong choice for supporting compliance with the new standards. Moreover, I believe the revenue and lease standards aren’t an aberration; they are harbingers of all future accounting standards.

Spreadsheets – the mainstay of accounting departments – are no longer a practical option for lease accounting unless an organization only has a handful of leases; most midsize and larger corporations have more than that. Indeed, large companies typically have hundreds and  even thousands of property and equipment leases in force at any time. Capturing all these data points accurately in desktop spreadsheets is problematic because of control and accuracy issues.

even thousands of property and equipment leases in force at any time. Capturing all these data points accurately in desktop spreadsheets is problematic because of control and accuracy issues.

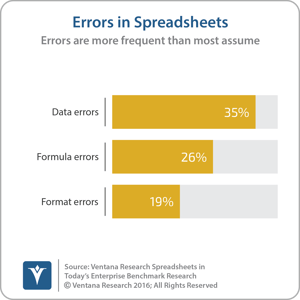

Spreadsheets have numerous inherent defects that make them unsuitable to repetitive collaborative enterprise tasks such as lease accounting. For example, our Spreadsheets in Today’s Enterprise benchmark research finds that more than one-third (35%) of participants have data errors in the most important spreadsheet they use in their work and 26 percent have errors in formulas. More than half (55%) of participants that use spreadsheets all the time in their work find there are multiple, inconsistent versions of the same spreadsheet circulating frequently or all the time.

Software designed specifically for lease accounting is the better choice. One important reason that’s easy to overlook is that the standards take a more principles-based approach to accounting. Principles-based accounting puts a premium on the consistency of the accounting and places controls on accounting processes to ensure that consistency. Enterprise computing systems bake in this consistency. Such systems also serve as a high-level control that can reduce audit hours, especially for U.S. companies covered by the Sarbanes-Oxley Act.

As companies work to master the complexities of the new lease accounting standards, it’s important for them to focus on having the right systems and software to make operationalizing compliance with the new standards as efficient and easy as possible. Otherwise, three aspects of the new standards are likely to cause burdensome accounting workloads.

First, under the new standards leases must be reviewed regularly. Typically, property leases – office space or retail stores, for example – account for the majority of the lease obligation value and almost always have non-standard terms and conditions. Changes in lease terms (such as cancelling the lease or adding options to renew) or even some business circumstances (for instance, losses at a retail location that makes a lease renewal unlikely) require accounting adjustments and remeasurements. So companies need to have systems in place that make it easy to set up and perform periodic review processes, make changes and record those changes in a system of record while providing continuous control and oversight to the process. This means having software to manage the process and a database-of-record to simplify access to and reporting on the relevant information.

Second, because separate departments in multiple locations are likely to perform lease management and lease accounting processes, it’s essential to use a dedicated application to tightly integrate these processes so that the accounting department can capture all leasing events and related data as they occur. To manage this integration it would be best to have software that streamlines the process of capturing that data correctly and consistently and provides alerts when some lease-related event requires attention. This ensures accuracy, auditability and compliance. The alternative – using email to transmit the information and spreadsheets to perform the calculations – makes it difficult to ensure accuracy, is likely to be far more time-consuming and will almost certainly require greater (and more expensive) effort by external auditors to confirm that the financial statements are correct.

To illustrate why the new standards require a dedicated application, let’s say that one year into a three-year lease the logistics department in the western division of XYZ Company decides to accept a new offer by the lessor for an option to extend the lease on a warehouse by another three years. In the past this would have been a non-event from an accounting perspective. Now, the accounting department must have relevant details of the change in the lease agreement. Even though XYZ hasn’t exercised the renewal option, new standards require the company to immediately recalculate the value of the lease to reflect this option, create a set of journal entries to capture that change and show a higher lease liability on its balance sheet. The remeasurement of the lease requires a set of computations to calculate the present value of future lease payments. These computations can be complex, but even when they’re straightforward they can be difficult to do consistently and accurately using spreadsheets.

Centralizing the lease-management function into a “center of excellence” is one approach to dealing with lease management issues but it won’t eliminate the need for dedicated software. In larger organizations a center of excellence can produce operational savings by, for instance, standardizing leased-equipment vendors to take advantage of bulk discounts or establish a better negotiating position. A group focused on lease management often can do a better job than those groups that only occasionally need to handle leases. Yet financial executives should keep in mind that although centralization addresses some of the operational issues and consolidates record keeping, it doesn’t get around the need to have software that holds that consolidated financial and non-financial data, manages processes, enforces compliance reviews, performs calculations accurately and consistently and streamlines financial statement disclosures.

Third, as I mentioned earlier, the new standards are designed to be principles-based. This gives businesses greater flexibility than a rules-based approach but it requires enhanced process and calculation controls to ensure consistency of accounting treatments. Accounting that is grounded more on principles and less on rules also requires more detailed disclosures about how the standards have been applied. Companies need a system to manage the process and workflows to ensure proper oversight. In addition, all lease-related data (not just accounting data) should be readily available to make reporting disclosures as simple and easy as possible.

Most companies will spend the next year or two using lease-accounting processes that are mostly manual and that are supported by masses of spreadsheets. All corporations must recognize that this approach imposes heavier-than-necessary workloads on their accounting departments.

Software is the answer. But selecting the right software to manage leases and handle their accounting is likely to be a challenge. There are many choices already and more will become available. Corporations that have reporting requirements under both US-GAAP and IFRS standards will need software that handles both because they are different. Some will find that the existing lease-management software used by the real estate department doesn’t adequately serve the needs of their accountants. ERP systems may be able to manage the accounting aspects of the process but may not be adequate for lease management or for easily collecting and updating non-financial lease data necessary for measuring the value of the lease.

As a starting point, I recommend that corporations focus on two objectives in formulating their approach to lease accounting and the software they use to manage the process. They should ensure that they can easily collect, retain and report all the data necessary for lease accounting. And because the process is cross-functional, they should balance the potentially competing needs of the participants in lease management and accounting processes.

Regards,

Robert Kugel

SVP & Research Director

To read more perspectives by Rob, visit https://robertkugel.ventanaresearch.com/

Robert Kugel

Executive Director, Business Research

Robert Kugel leads business software research for ISG Software Research. His team covers technology and applications spanning front- and back-office enterprise functions, and he runs the Office of Finance area of expertise. Rob is a CFA charter holder and a published author and thought leader on integrated business planning (IBP).