New standards governing accounting for contracts will go into effect for most companies in 2018. The Financial Accounting Standards Board (FASB), which administers Generally Accepted Accounting Principles in the U.S. (US-GAAP), has issued ASC 606, and the International Accounting Standards Board (IASB), which administers International Financial Reporting Standards (IFRS) used in most other countries, has issued IFRS 15. The two are very similar, and both will enforce fundamental changes in this area of accounting. Under the new approach to accounting for contracts, revenue (and some corresponding expense) is recognized only when customers are satisfied. In contrast, until now revenue was recognized when internally measurable events occurred, such as on delivery to the customer, the completion of milestones or the passage of time. In addition to dealing with an impact on accounting and planning, which I have discussed, companies may need to examine how the rules will affect how they account for commissions and other contract acquisition expenses.

The new accounting rules will affect all companies that enter into contracts with customers. For some (maybe a majority), the change will be more of form than substance. For them, the change can be handled readily by ERP and other accounting software that has been designed specifically to handle the new requirements. For instance, ASC 606 and IFRS 15 spell out a more elaborate, multistep process for booking contract revenue, but as I have noted, companies that design their contracting processes to facilitate accounting for them and use an application that automates the steps in the process will be able to substantially eliminate what otherwise would be an administrative burden.

On the other hand, the new accounting rules will have a significant impact on some corporations that use even moderately complex contracts in dealings with customers. They include, for example, contracts that are use tiered pricing or volume discounts, others that routinely involve modifications, such as adding or dropping services, or projects that require modifications in scope or term. Examples of the types of businesses most likely to be affected in this way include those in engineering and construction, ones that augment their products with recurring services as part of an ongoing relationship with customers (such as maintenance or consumable parts) and companies that offer subscription services that involve deliverables that can vary over time (such as units consumed or service levels).

The new standards also may affect how companies account for commissions. The new rules require companies to capitalize the incremental costs of obtaining a contract (such as sales commissions) at inception if the contract’s duration exceeds one year. This deferred expense is then amortized over the term of the contract so as to better match specific expenses to related revenues. However, not all expenses can be capitalized. For instance, compensation paid to supervisors, even when tied to sales volume, is expensed in the period incurred.

For contracts covering a year or less, companies will have to expense commissions immediately. It’s likely that auditors also will allow companies to immediately expense commissions and other contract acquisition costs even for contracts that extend beyond one year as an accounting policy election. However, this will be allowed only if a company applies this treatment consistently to all contracts with a term of one year or more and if the impact does not materially distort the financial statements.

Some companies may elect to expense all sales commissions immediately to keep things simple. This is more likely if a large majority of business done with contracts is fulfilled in one year or less; if commissions and other contract acquisition costs are relatively small; or if the company is closely held. However, others – especially publicly listed companies – may decide that capitalizing sales expense provides a more accurate picture of their financial performance, especially if comparable companies take this approach to their accounting. Under these circumstances, I recommend using sales compensation management software to track sales commissions. This type of application already offers considerable value to sales organizations. For companies that will capitalize commissions, sales compensation management software is likely to reduce accounting and auditing workloads substantially for those that have used spreadsheets to do it.

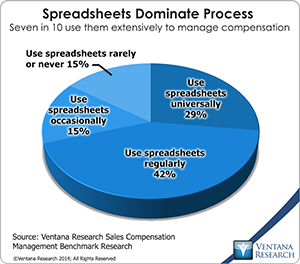

Our sales compensation management benchmark research finds that a large majority (71%) of companies use spreadsheets  universally or regularly to manage their sales compensation process. Yet 61 percent of participants said that spreadsheets make it difficult to manage sales commissions, and nearly two-thirds (65%) said that the commission calculation process is too slow. Moreover, companies that capitalize sales expense and enter into even moderately complex contracts with customers are likely to find that using spreadsheets to manage sales compensation will multiply the workload of the accounting department.

universally or regularly to manage their sales compensation process. Yet 61 percent of participants said that spreadsheets make it difficult to manage sales commissions, and nearly two-thirds (65%) said that the commission calculation process is too slow. Moreover, companies that capitalize sales expense and enter into even moderately complex contracts with customers are likely to find that using spreadsheets to manage sales compensation will multiply the workload of the accounting department.

Under ASC 606 and IFRS 15, managing sales compensation in spreadsheets will increase the burden of accounting departments in several respects. Because spreadsheets are error-prone, accountants will need to check all of them to ensure that amounts and calculations are correct. Even assuming that the sales organization will attempt to be diligent in allocating commission and other direct contract acquisition costs appropriately between those that are to be capitalized and those that are to be expensed, accountants will still have to check the work to be certain that no mistakes were made. In the event that changes to a contract affect the commissions paid, ensuring that this information is captured accurately in a spreadsheet and in a fashion that facilitates accounting can be a challenge. Manually posting transaction data taken from a spreadsheet is time-consuming and almost guaranteed to contain errors that will require a reconciliation process to identify. Even if the accounting system has the ability to automate posting transactions using data contained in spreadsheets, checks and reconciliations may be necessary to ensure the process was handled accurately. Moreover, because spreadsheet-based systems are inherently less controlled, they require greater scrutiny by internal and external auditors.

In contrast, sales compensation management software can prevent such issues from occurring. It can simplify tracking of the exact amount of commissions paid on contracts that extend past one year and reliably distinguish between amounts paid to supervisory personnel and commissions paid on contracts with a term of one year or less. The system can be programmed to capture all relevant characteristics of the transaction, automatically calculate commissions and incentive payments, and allocate amounts according to the required accounting treatment. In some companies, complications to accounting for commissions can arise when, say, area managers collect both direct sales commissions (which may be capitalized) and when they receive incentive compensation based on the performance of their direct reports (which must be expensed). Compensation management systems can easily keep these two types of payments separate. Complications can also arise if a contract is extended or modified in a way that will affect the amount and treatment of commission payments. Here also sales compensation management systems can track these changes in a way that facilitates accounting for them. Moreover, having a dedicated system makes it possible to fully automate the posting of all relevant information into the company’s accounting system on whatever schedule, form and format the accounting department prefers. This eliminates the need  for manual data entry and ensures accuracy and timeliness.

for manual data entry and ensures accuracy and timeliness.

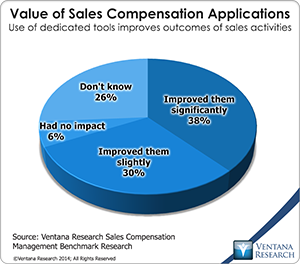

Facilitating the accounting for capitalized commissions under the new revenue recognition rules is just one reason why we recommend that companies evaluate sales compensation management software. Our research finds that 38 percent of those that use dedicated sales compensation software said they have significantly improved the outcomes of their sales activities and processes. Another 30 percent said they have improved them to some degree. A dedicated application also processes commissions faster and more accurately, which can help retain productive sales people: More than half (57%) of companies said they can handle them in less than a week. Another, more sophisticated benefit is that the sales force is aligned to business strategy and goals, which 43 percent ranked first, more than any other benefit of such software. Other benefits cited are better management and tracking of the progress of product and sales initiatives (by 30%), improved communications to Sales on the status of compensation (26%) and improved auditing and compliance of sales forecasts to goals and targets (25%). Among those planning to adopt dedicated sales compensation management. the highest-ranked expected benefits are to increase revenue and grow the business in terms of net new customers.

We recommend that companies that use spreadsheets to manage sales compensation investigate the benefits of using a dedicated application. The potential impact of the new rules for recognizing revenue from contracts adds another reason why a dedicated application can improve the productivity and performance of both the sales and accounting organizations. As for corporations that already use sales compensation management software and will be affected by the new accounting rules, ensure that the systems are set up to facilitate handling accounting tasks in this new environment.

Regards,

Robert Kugel

Senior Vice President Research

ISG Software Research

ISG Software Research is the most authoritative and respected market research and advisory services firm focused on improving business outcomes through optimal use of people, processes, information and technology. Since our beginning, our goal has been to provide insight and expert guidance on mainstream and disruptive technologies. In short, we want to help you become smarter and find the most relevant technology to accelerate your organization's goals.